How Battery Health Reports will support remarketing of used Battery Electric Vehicles (BEVs)

The battery electric vehicle (BEV) is a crucial building block in vehicle manufacturers’ mission to meet Europe’s CO targets. A strong supply of BEVs, which are currently heavily subsidized on the new-car market and which will mostly register through leasing agreements, will create a strong supply of used cars three to four years down the road.

Extended warranties for batteries merely represent a way to stop losses from a used-car buyer perspective: in the absence of certainty around replacement costs, these warranties help avoid a worst-case scenario where BEVs would become almost unsellable.

Another substantial market risk (and market opportunity) is the treatment of the battery. Whether a battery is treated well or not – keeping all other factors such as climate, geography, topography and mileage as constant, can result in an approximately 5% difference in quality (e.g. range) in a battery after three years and a distance of 45,000 km.

Treatment factors considered for a simulation were driving, charging and parking behaviour. Without transparency regarding the battery treatment (and operating conditions), the battery quality cannot be correctly evaluated. This further emphasizes the substantial information asymmetry between seller and buyer. The buyer assumes the worst quality and the seller has no incentive to treat the battery well. This inevitably creates a downward spiral.

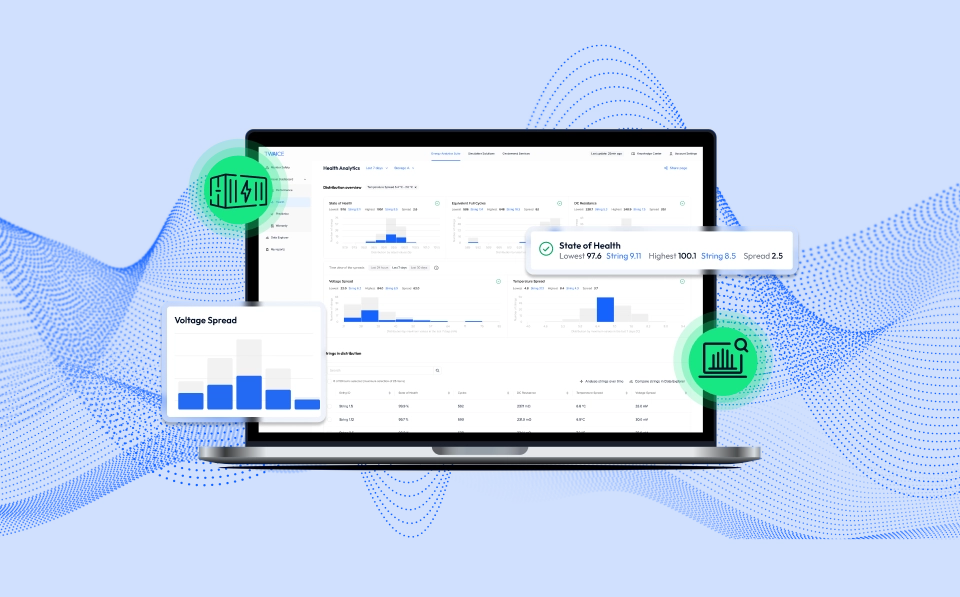

Improved and verifiable battery quality can deliver approx. 2.4% additional value in the transaction, i.e. approx. €450 for a three-year used C-segment BEV in Germany. Effective signals in the form of Battery Health Reports (BHR) can create economic value of €4.5 million for every 10,000 BEV used-car transactions – to the benefit of all stakeholders. Sellers of BEVs should remarket the vehicle with a Battery Health Report (BHR) to eliminate the information asymmetry.

This information should be available as a standard data item on used-car portals, similar to information on age, mileage and equipment. Leasing companies could manage better or worse treatment in a similar way to how they treat lower or excess mileage, again to the benefit of all stakeholders.

The TWAICE-TÜV Rheinland joint venture Battery Quick Check offers a battery health certificate. A detailed product description and explanatory videos are available on their website.